Retail media vs trade marketing - what's in your revenue number

Most retailers look at a retail media revenue figure. Very few know what's genuinely in it - or whether it represents real commercial growth. Here's how to tell the difference.

Quick answer

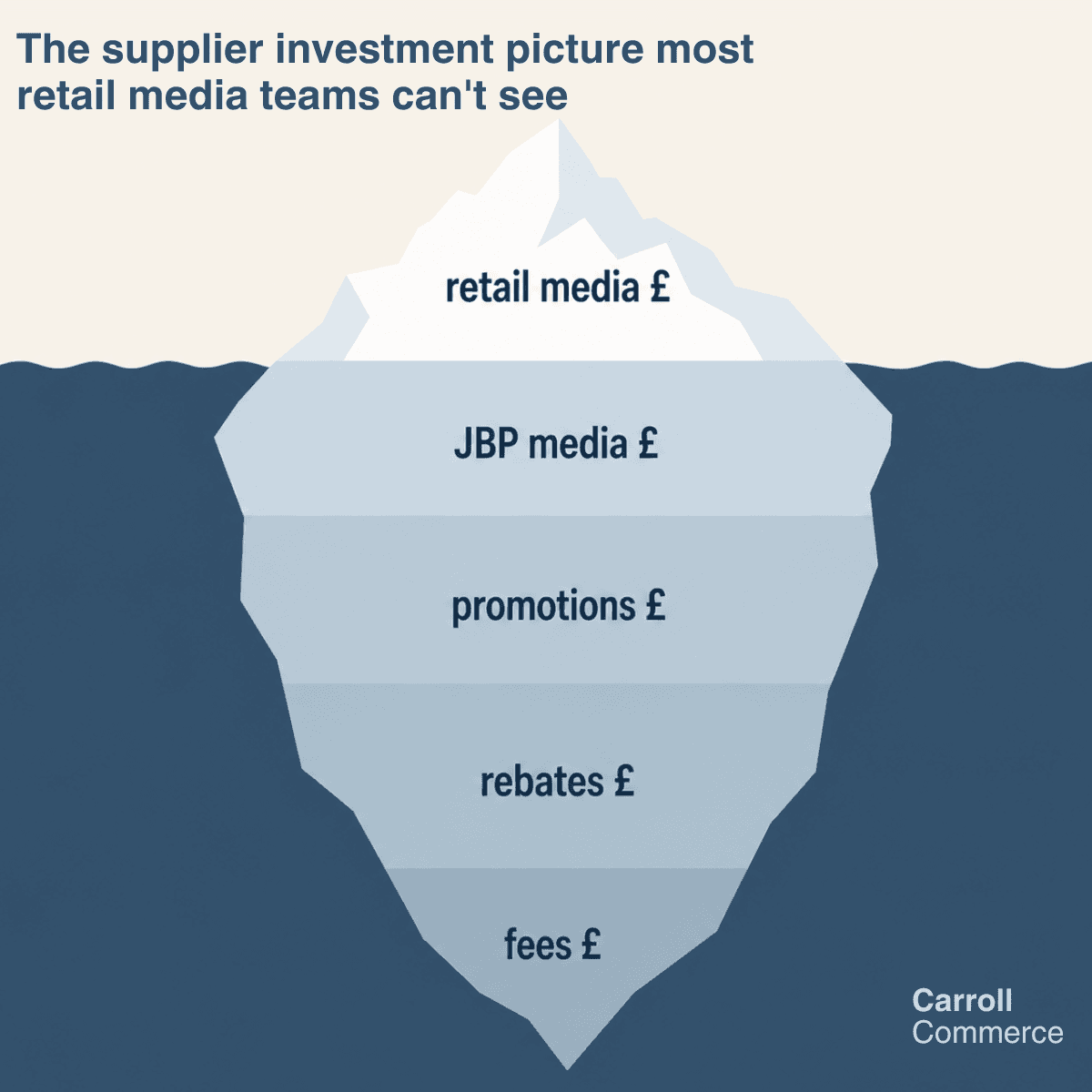

Retail media and trade marketing are not the same thing, but in most retailers they live in the same pot. The result is a revenue number that looks bigger than it is and makes it almost impossible to answer the only question that matters: is this genuinely new money, or just old money with a new label? Getting this right is one of the most important - and most overlooked - steps in building retail media properly.

Three terms, one confused conversation

Before getting into the numbers, it helps to be clear about what these terms actually mean - because in many retail organisations they are used interchangeably, and that imprecision is part of the problem.

Trade marketing is the broadest term. It covers everything a brand invests with a retailer to support their commercial relationship - listing fees, volume rebates, promotional funding, price support, marketing fees. Much of it is contractual, negotiated annually in the Joint Business Plan (JBP). It is primarily a commercial function conversation, buyer to account manager, and it has existed as long as modern retail has.

Shopper marketing is a subset of trade marketing focused specifically on influencing the shopper at or near the point of purchase. End-of-aisle displays, floor stickers, sampling stands, in-store events, printed leaflets, digital screens at shelf. It is more marketing-oriented than pure trade - there is usually a creative agency involved, a brief, a campaign idea. It emerged as a discipline in the 1990s and 2000s as brands got more sophisticated about the last mile of the purchase journey. But it is still largely funded from trade budgets and negotiated as part of the commercial relationship.

Retail media is what happens when you apply digital infrastructure, first-party data, and closed-loop measurement to the same commercial relationship. It can cover on-site sponsored products, off-site audience targeting, and in-store digital screens - and when it is done properly, every element is measurable, targeted, and tied to outcomes rather than just presence.

Where it gets blurry

In-store digital screens are a good example of where all three converge. A digital screen at the end of an aisle could be shopper marketing - if it is sold as a fixed tenancy, designed by a creative agency, funded from trade budget, and measured by footfall past the screen. Or it could be retail media - if it is sold programmatically, targeted using data to show different creative to different shopper profiles, and measured by sales uplift in the category. In theory.

In practice, many retailers are selling screen inventory as retail media simply because it sits on a digital screen and can be centrally managed - even without programmatic buying, targeting, or sales measurement. Which makes the definitions even messier than the theory suggests.

This is why many retailers have a messy revenue number. The same screen, the same supplier relationship, and sometimes the same invoice can be classified differently depending on who is managing the relationship and how the contract is written. Shopper marketing sits between old-school trade and modern retail media - and the difference is not the format, it is the measurability, the targetability, and whether the data infrastructure underneath it can prove what the spend actually drove.

There is another layer of complexity worth naming. Retail media is often bought through media agencies, who may hold the purchase orders even when the investment decision came from the brand. One agency can represent multiple supplier brands simultaneously. Getting a clean view of total supplier investment therefore requires linking agency spend back to individual brand relationships - a data problem that most retailers have not yet solved, and one that rarely appears on anyone's priority list until the revenue numbers stop making sense.

The benchmark question every C-suite asks

Every retail C-suite wants a benchmark: what percentage of total revenue should retail media be hitting?

It is a reasonable question. A quick read on how well the business is monetising its media assets and how large the opportunity might be.

The problem is that the answer is more complicated than most people think — and the benchmarks that get quoted are often comparing things that cannot meaningfully be compared.

Look at the two retailers most commonly cited as retail media leaders. Amazon Ads generated $17.2 billion in Q1 2026 — 9.48% of net sales. Walmart Connect revenue was nearly $6.4 billion for FY2025 — 0.94% of retail sales. That is a tenfold difference between the two most advanced retail media businesses in the world.

But comparing them directly tells you almost nothing useful. Amazon is primarily an ecommerce marketplace where advertising is structurally embedded into search and discovery. Walmart is a predominantly physical retailer building its digital advertising business. Different format. Different data maturity. Different category mix. Different customer behaviour.

For UK and European grocery retailers, disclosed retail media revenue figures are largely absent from public reporting. Which means industry benchmarks are built on incomplete and often estimated data.

So what is actually useful? Not market vs market. Not retailer vs retailer at total business level. The better approach is to do the work - assess demand and supply in ways specific to your business, and triangulate to get a credible range. And the most meaningful benchmark is not a percentage of total revenue. It is whether total discretionary brand investment is genuinely growing - and whether retail media is an additive part of that, or simply a reallocation of money that was already flowing.

The problem nobody talks about: the view of the money

When I was in a global retail media role, I visited markets across Latin America, Asia, and Europe. About eighteen months in, revenue was not scaling as planned. My job was to understand why.

I started to notice a pattern.

More than once, I arrived to find that in the days before my visit there had been a sudden flurry of retail media sales. The market was miraculously hitting its monthly target. Until I got nosey.

What had actually happened: the commercial team had fired off a few messages to their most accommodating suppliers and shifted some JBP investment budget out of promotions or tenancy media and into programmatic retail media. Job done. Everyone looked good for the person coming from HQ.

I don’t blame them; they had a day job and targets to hit. Retail media was new and complex. But it exposed a structural problem that I see repeatedly in retailers at every stage of retail media maturity.

Why clean numbers matter

If you are a retailer, you need to be very clear about what retail media revenue is and is not. And that money needs to be clearly visible - separate from front margin (trade price) and back margin (rebates, promotional funding, listing fees) - so you can see what is real and hold the right people accountable.

When it all sits in the same pot, the money lines get blurred.

And even a clean retail media number on its own is not enough. A supplier can look like a retail media growth story while quietly reducing promotional investment by the same amount. Who has visibility of the whole picture and is asking whether the total grew?

A good commercial director might look at total supplier investment. Many do. But that is one person, with their own targets, looking at their own domain. It is not a scalable structure for building a retail media business.

The right question to ask

To know whether retail media is genuinely additive, you need to look at the bigger picture - total discretionary investment at brand level. Promotional funding, volume rebates, marketing contributions, and retail media combined.

If retail media is up but the combined pot is flat, you have not created new value. You have moved money between columns.

Most retail media teams cannot answer the question "is this genuinely additive?" That is a problem worth solving before you set targets, before you benchmark against Amazon, and before you report a retail media revenue number to your board.

In that global role with a bird's eye view across markets, I would pull the top performers on retail media revenue as a percentage of general merchandise value (revenue from items sold). Some markets looked exceptional - until you looked at total margin across front margin, back margin, and retail media combined. The story could change completely. Markets doing best on retail media were not always the most commercially healthy. Some of the apparent laggards were quietly generating strong margin through other levers.

The benchmark was real. But the story it told was not.

What to do instead

Getting a clear picture of existing money is the essential first step. Before setting targets or benchmarking, answer these questions:

What is already flowing between your commercial teams and brand partners? What counts as trade spend and what counts as media? Are your definitions consistent across categories and markets?

Then get granular. Identify your top 50-100 suppliers. Understand what it would take for each of them to invest in retail media as genuinely incremental spend. Run pilots, test and learn, and aim to land larger commitments at the next annual JBP cycle with clear visibility of the full investment picture.

The retailers building retail media properly are the ones working toward this level of visibility - not the ones with the biggest headline number. To be honest, very few have fully cracked it yet. But the ones who are asking the question are already ahead of the ones who are not.

The only sustainable model: make it work for brand partners too

There is one more thing that rarely appears in retail media revenue conversations, and it is the most important of all.

If your brand partners are not generating genuinely incremental business from their retail media investment - new customers, recovered lapsed buyers, measurable sales uplift - they will eventually stop investing. The money might stay in the JBP for a cycle or two out of inertia or relationship. But it will not grow. And it will not be additive.

The only way to build retail media revenue that compounds over time is to make it genuinely valuable for the brands investing in it. That means closed-loop measurement they can trust. It means audience targeting that reaches people they could not reach elsewhere. It means category and shopper insight that makes their broader business better. It means being honest when a campaign did not perform and working out why.

This is not altruism - it is commercial logic. A brand partner who can point to real business outcomes from their retail media investment will come back with a bigger budget next year. One who cannot will quietly reallocate.

The retailers building sustainable retail media businesses are the ones asking not just "how do we grow our retail media revenue?" but "how do we make retail media genuinely valuable for the brands investing in it?" The answer to the second question is what makes the first one possible.

Who this is for

Carroll Commerce works with retail CEOs, CCOs, and commercial leaders who want to build retail media as a genuine business rather than a revenue line that obscures more than it reveals. If you are trying to get clarity on what your retail media number actually means - and what it could be - get in touch with Tara Carroll.

FAQ: Retail media vs trade marketing

What is the difference between retail media and trade marketing?

Trade marketing covers the promotional investment brands make with retailers - end-of-aisle displays, price promotions, volume rebates, listing fees. It has existed since the 1990s and is typically negotiated between commercial teams. Retail media uses digital infrastructure and first-party data to make brand investment measurable and targeted, connecting spend directly to sales outcomes. The two often coexist inside the same retailer and are frequently reported as a single number - which creates significant visibility problems.

Why do retailers combine retail media and trade marketing revenue?

Historically the commercial teams managing trade spend and the teams building retail media sat in different parts of the organisation, but both relationships lived with the same brand partners. As retail media grew, it was often easier to report a combined "supplier investment" number than to separate the two cleanly. The result is that many retailers have a retail media revenue figure that includes reclassified trade spend - which makes the number look bigger than the genuinely incremental retail media opportunity actually is.

What is JBP reclassification and why does it matter?

JBP stands for Joint Business Plan - the annual commercial agreement between a retailer and a brand partner that covers trade investment, promotional spend, and increasingly retail media. JBP reclassification happens when money that was previously classified as promotional spend gets moved into retail media without any net increase in total brand investment. The retail media number goes up, but no new value has been created. This is one of the most common ways retail media revenue figures get inflated.

How should retailers measure whether retail media is genuinely additive?

The most reliable approach is to track total discretionary investment at brand level - promotional funding, volume rebates, marketing contributions, and retail media combined - over time. If retail media is growing but the combined pot is flat, the money has been reclassified rather than grown. Genuine additionality means the total investment from brand partners is increasing, with retail media as a net new contribution rather than a reallocation.

What is a realistic retail media revenue benchmark for UK retailers?

There is no reliable published benchmark for UK grocery retailers - most do not disclose retail media revenue separately. The most meaningful benchmark is not a percentage of total sales but whether your retail media revenue is genuinely incremental to total brand investment. Getting a credible view of the opportunity requires assessing your specific customer data, supplier base, and category mix - not benchmarking against Amazon or Walmart, which operate fundamentally different business models.

Why do brand partners eventually stop investing in retail media?

Brand partners reduce or reallocate retail media investment when they cannot demonstrate that it generated genuinely incremental business outcomes - new customers, recovered lapsed buyers, measurable sales uplift. Without closed-loop measurement, credible audience targeting, and honest performance reporting, retail media becomes indistinguishable from other media buys that brands can make more cheaply elsewhere. Making retail media work for brand partners is not optional - it is the commercial foundation that makes retailer revenue sustainable.